In 20 years’ time we’ll be just a year away from the Government’s ban on the sale of new petrol and diesel vehicles. By 2039, the demand for electric and hydrogen-powered vehicles will have fundamentally reshaped the automotive landscape. The infrastructure to support them, charging networks, hydrogen refuelling stations, grid capacity, will have matured dramatically, but the transition won’t have been smooth for everyone.

Subscription-based mobility services will have replaced outright vehicle ownership for a significant portion of the population. Flexible working patterns, accelerated by the pandemic, will have reduced the need for a second household car. Consumers will subscribe to a vehicle when they need one, swapping models based on lifestyle demands, a city car during the week, an SUV for the weekend.

Commercial vehicles will have undergone an even more radical transformation. With road transport responsible for a significant share of greenhouse gas emissions, regulation will have forced the industry toward zero-emission fleets. Load sharing, route optimisation, and autonomous last-mile delivery will be standard. The economics of fleet operation will look entirely different.

Welcome to Legislation Nation

EV ranges will comfortably exceed 400 miles, and charge times will have dropped below five minutes for an 80% top-up. Urban restrictions on internal combustion vehicles will be widespread, with many city centres operating as zero-emission zones. Night-time delivery windows will have expanded as autonomous vehicles handle the bulk of urban freight outside peak hours.

Road charging will have replaced the revenue previously generated by Benefit-in-Kind taxation on company cars. As fleets electrify and BIK yields collapse, the Government will have implemented per-mile road pricing, variable by time of day, congestion level, and vehicle type. This will reshape fleet management strategies entirely.

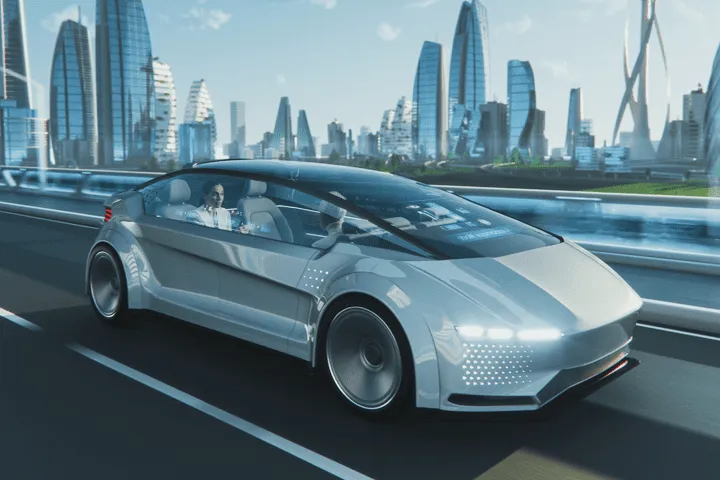

Ride-hailing services will have evolved beyond recognition. Vehicles will be permanently connected, booking their own service appointments, reporting faults in real time, and negotiating with infrastructure networks autonomously. Higher speed limits on designated autonomous corridors will have been introduced, improving journey times on major routes.

Level 5 fully autonomous vehicles will exist, but Government restrictions on their deployment will remain cautious. The insurance liability shift, from driver to manufacturer, will have been the single biggest legal and commercial renegotiation in the sector’s history. OEMs, insurers, and regulators will still be working through the implications two decades on.